Succumbing to hype? An emotional history of investing

An investor’s emotions can become their worst enemies, especially when – as now – we appear to be living through successive crises and unprecedented change. How can we rein in our emotional responses to events? History provides some fascinating insights.

Authors

The world is still in the grip of an unprecedented pandemic. Daily headlines highlight economic shocks, debt crises and other alarming financial, social and environmental news. With this as a background, how can investors – who may be worrying about existing holdings as well as considering how to introduce new cash into the market – find reassurance?

History has some of the answers. It shows repeatedly how human emotions have led to some of the most dramatic financial losses. History also demonstrates, by contrast, that a planned approach to investing – which often entails stepping back from the “noise of now” – is a demonstrably more successful strategy.

Fear and greed over the centuries

Wind the clock back to 17th century Holland, where global trade was driving rapid change and where investors were hungry for short-term profits. A taste for exotic plants gripped wealthy society. But “tulip mania” – as the craze for tulips, then a new plant in western Europe, became known – was also a financial phenomenon.

Investors not only traded feverishly in tulip bulbs themselves, but they also traded in tulip “futures” – paper contracts that promised the owner delivery of a certain type of tulip bulb on a certain future date. As these contracts flew from hand to hand, prices were cranked up even higher.

Often referred to as the first “bubble”, tulip prices soared in the 1620s and 1630s, with single bulbs attracting prices that were multiples of annual wages and exceeded the value of large properties.

Inevitably, investors’ exuberance soured. In February 1637 fear set in. Buyers vanished in the course of a few days and prices crashed.

Fashion, greed, rarity: the factors that caused tulip prices to blossom

Notes and sources: *Asking prices / achieved sales prices for a single bulb of tulip variety Semper Augustus: multiple sources. Today’s approximate values calculated by comparing the ratio of tulip prices to skilled labour wages in 1630s Holland to skilled UK labour prices today (source: ONS May 2021).

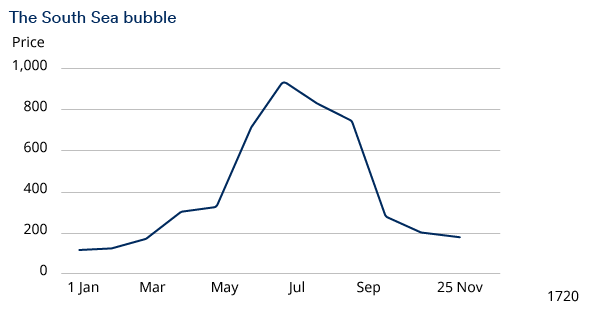

A century later in 1720s Britain something similar occurred with shares in the much-hyped South Sea Company. The idea was that the company would profit hugely from trade with Spanish America. It would also take on part of Britain’s national debts, distributing the Government’s interest payments to shareholders as part of their dividend.

With King George I as governor of the firm, confidence was high and shares hugely promoted. Share prices rose almost tenfold in the first half of 1720, fuelling a speculative frenzy in which it was claimed even “the greatest ladies... pawned their jewels… to venture in the [Stock Exchange] Alley”.

A stream of other “bubble companies”, purporting to profit from more or less feasible schemes, followed suit, attracting both followers and derision. Historians claim many buyers were entirely cynical, hoping to profit in the short-term by finding credulous “investors” who would pay even higher prices. Others appeared to genuinely believe the hype around the company’s potential success.

By September 1720 South Sea shares had collapsed, ruining many and sparking a political crisis.

South Sea investors: lured by hype and hope of a fast profit

Notes: Monthly traded prices in £ per £100 face-value of stock. Multiple sources.

Emotional rollercoasters in the 21st century

Back to the 21st century and few investments today spark as much controversy as bitcoin, which has attracted powerful fans as well as critics. The soaring price of bitcoin – and its frequent reversals – have led to many comparisons with historic bubbles.

Bitcoin’s critics argue that investors see it as a source of short-term gain on the “another fool principle” – the idea that other buyers can be persuaded to shell out yet more in the future. The question of whether it has any intrinsic value or use, is also hotly debated.

Cazenove Capital has examined bitcoin and to date, we’ve chosen not to invest in it, although we do see huge potential in the technologies which underpin some cryptocurrencies.

What is undeniable is the volatility of bitcoin, which has seen some staggering surges and setbacks in value.

Bitcoin’s rises and falls: a picture of 21st century fear and greed?

Source: Refinitiv, 25 May 2021

The danger of short-termism

Bitcoin, tulips and celebrated investments such as the South Sea Company have features in common. In all cases there is a powerful story, often told in colourful and emotional language. There is an urgent sense of a one-off opportunity; and also of the danger of losing out where everyone else is scoring huge profits.

It can be difficult to resist participating in the face of this barrage of persuasive and emotive information. Known as “herding”, the common response of individuals is to go with the flow. But doing so can lead investors to poor decision-making and financial loss. It can be particularly dangerous where investors are trying to save for long-term objectives such as retirement.

Again history proves instructive. Take a very recent example: the collapse of markets following the rapid spread of Covid-19 in early 2020.

Once it became clear that Covid-19 would have a severe impact on economic activity, investors fled and stocks suffered a dramatic global slump. And it is true that any long-term investors who followed suit and sold their holdings may have limited some of the short-term loss.

But they would also have missed out on what was an extremely rapid recovery. In fact, markets went on to reach record highs in the following months.

The chart below is a stark warning of the dangers of herding. It shows that 2020’s collapse was the most dramatic of recent collapses, in that markets fell by 20% more rapidly than in any of the other cases. But it also shows that the recovery (in terms of months, see right-hand side) was also among the quickest.

Past performance is not a reliable predictor for future results.

Source: Refinitiv, Schroders, Data based on Datastream World Stock Market index, 1 January 1973-30 November 2020. Days are measured in trading days, not calendar days. All analysis is based on returns in US dollar terms. Months for investors to make their money back assumes that investors have remained fully invested throughout. YTD data based on MSCI equity indices. Data covers 31 December 2019 to 30 November 2020 period. 601688

If you sold when everyone else was selling, you would also have to know when to buy in order to benefit from the subsequent recoveries. In 2020 it took just five months for markets to recover, even after a peak-to-trough fall of over 30%. Even in the worst of recent collapses (2009, where the decline was 58%) the period to recovery was well under five years. Those who held on during the trough periods – or, better still, continued to contribute money to the markets – would have seen their holdings recover fully in value or indeed would have made further gains.

Would you be tempted to invest in the 21st century equivalent of tulip bulbs? Quite possibly, but if you turned first to your plan you might pause to consider just how much you could afford to lose. And would you be tempted to sell your holdings after a market shock? You might, but again a look at your long-term plan might remind you that while markets can fall sharply – they can also bounce back with unexpected speed. In short, drawing up a long-term plan for what you want your money to achieve can be one of the best ways of saving you from yourself.

This article is issued by Cazenove Capital which is part of the Schroders Group and a trading name of Schroder & Co. Limited, 1 London Wall Place, London EC2Y 5AU. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Nothing in this document should be deemed to constitute the provision of financial, investment or other professional advice in any way. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested.

This document may include forward-looking statements that are based upon our current opinions, expectations and projections. We undertake no obligation to update or revise any forward-looking statements. Actual results could differ materially from those anticipated in the forward-looking statements.

All data contained within this document is sourced from Cazenove Capital unless otherwise stated.

Authors

Topics